.svg)

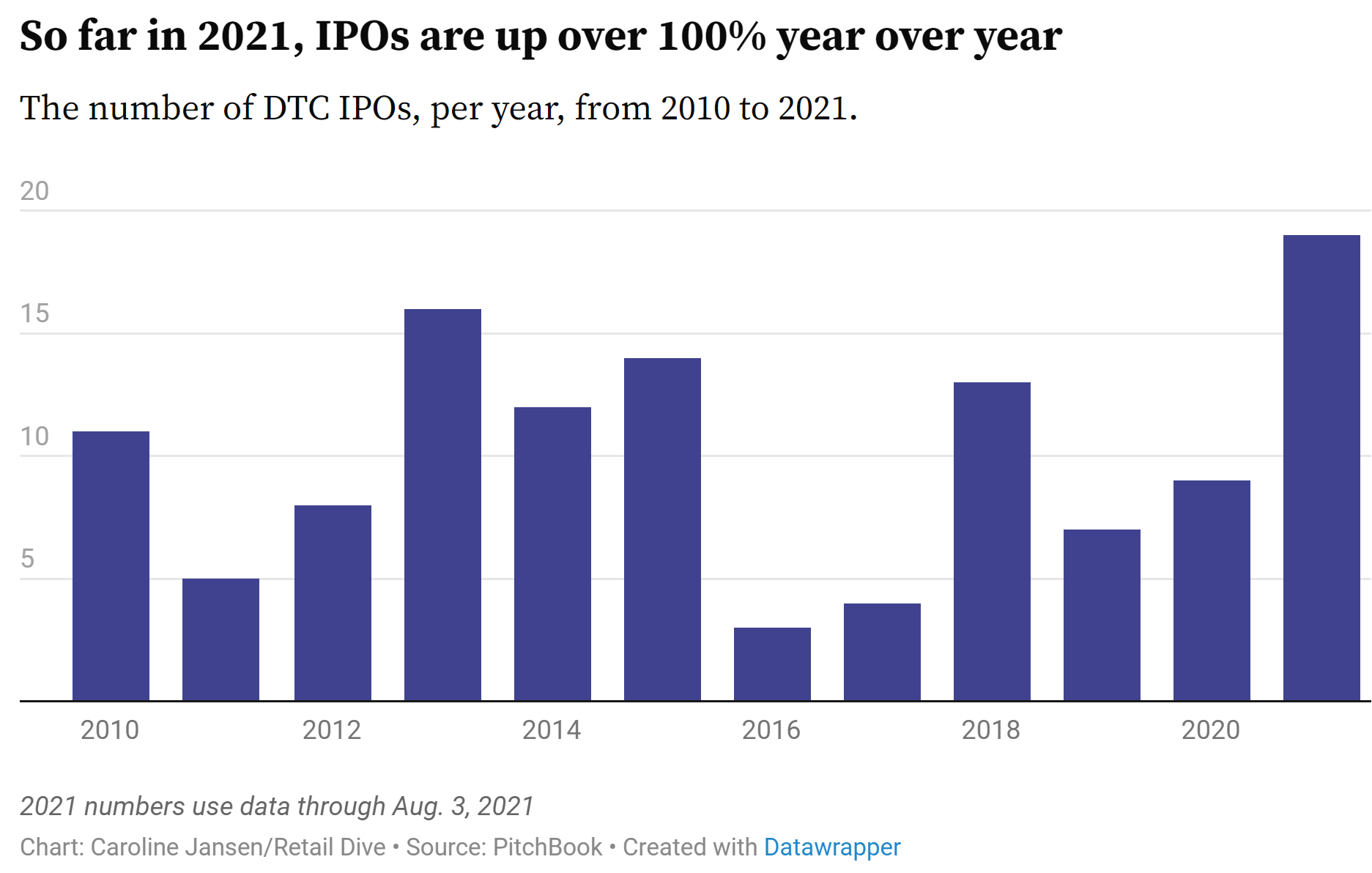

I. DTC is Dead some say, as many darlings of the early aughts and the 2010s have failed to yield as many durable companies as once expected. From 2008 to 2020, VCs invested approximately $20 billion in 1,500 companies which produced companies like Casper, Allbirds, Rent the Runway, Warby Parker, Chewy, Peloton, Glossier, Dollar Shave Club, Wanelo, Honest, Stitch Fix, Purple, Hims, Bonobos, Figs, and more. About 20 DTC companies IPO’d as part of the froth of 2021 market exits. DTC was part of the great and growing disintermediation that came with the internet. Direct-to-consumer was thought to be revolutionary because it offers benefits such as increased profit margins, enhanced consumer relationships, and an increase in data-driven insights. By leveraging technology and engaging directly with consumers, brands would have the opportunity to disrupt traditional industries and provide more personalized experiences. Further, visionaries like Kirsten Green at Forerunner went further.

DTC growth was not only about disintermediation but also a manifestation of a new psychological reality within commerce. Green made a name for herself by identifying retail companies that became breakouts during peak mall. But she built a real point of view around the idea that continued growth in disposable income would translate to unique growth in discretionary spending, which then would translate to a more discerning consumer, equipped with the transparency of the internet, that would thus be more and more powered to search for her thing. This thesis was buttressed by the second wave of DTC companies that focused on experiential or cultural components to drive value and compete with incumbents. Olipop. Fly By Jing. Mid-Day Squares. Hanifa. Topicals. Hero Cosmetics. The Honey Pot. These companies highlight Green’s view, and many others like Maveron, H Ventures, Selva who have also formed funds around the evolving retail landscape.

As the 2nd wave of DTC companies has come to the fore, a new understanding surfaced. DTC was never a revolutionary model per se, rather it is simply one of many retail channels that effective merchants must employ. If even the Big Smile company is focused on omnichannel distribution, how could it be prudent for any individual brand to be unichannel? Today, leading “DTC” brands must be as adept at their wholesale operations as they are at managing their influencer, YouTube, and agency playbooks. “DTC” — the idea that a brand can strangle the physics of the retail success equation by exchanging one form of intermediary (the slotting fee) with another (elevated CAC and distribution fees) is dead.

II. Those Headless Omnicommerce Tools. The efficacy of DTC as a channel didn’t lie just in its ability to expand discovery and reduce reliance on middlemen and commerce gatekeepers. Internet-based direct-to-consumer, or as Andy Dunn described it digitally native brands, also benefited from the massive amount of friction reduction related to brands’ success equation. Merchants want to increase revenue relative to the costs incurred to enable discovery, payments, record keeping, and fulfillment of their products. Companies like Finix, Stripe, Adyen, and Square have redefined the concept of the cash register or point of sale. Amazon, Shopify, and Faire have redefined and are redefining many dimensions of discovery. But they’ve also enabled a host of tools to be built as part of their ecosystems.

Modern retail has demanded an unbundling of powerful tools like the single enterprise resource planner or the customer relationship management system. This is not merely a question of monolith vs. microservices or large upfront costs and a horde of AE’s vs. PLG… The fundamental psychological and economic sea change has come from the internet’s undeniable forcefulness on our lives with a dimachaeri-like wielding of cloud and mobile infrastructure that increasingly leaves nearly no merchant standing in analog. Regardless of size, and especially after COVID, merchants, citizen-merchants, and enterprises are all increasingly digitally literate at the very least. This means more and more merchants are relying on more and more digital tools to run their basic business.

Data management and discovery are folding more and more into each other, as merchants rely on tools to pinpoint their customers and stand out among an ocean of consumer options.

When we were younger, we would spend part of our summers passing out flyers for Sola’s dad’s tax business. In the windshield wipers, a knock on the door, or in your mailbox… By any means necessary, the 7.5 of us were going to give 8 thousand flyers to 8 thousand people so we could have our CiCi’s pizza covered for the weekend. A small business logistics and tax company could not afford to pay SAP or Oracle installation costs of $25,000 to $300,000 plus an integration fee, plus a subscription just to get started. For decades, this meant a slow painful march towards inevitable digitization. Toast, Mindbody, Rippling, Slice, Shopify, Squire Technologies, Hubspot, Ramp have ridden the tide of bringing businesses of all sizes into the 21st century. According to the SBA, as of March 2023, there were 33,185,550 small businesses in the US, employing 61.7 million people, or 46.4% of the private sector workforce.

The tools and go-to-market motions that worked for pioneering startups focused on SMBs are starting to shape the nature and viability of ISVs more broadly, with a focus on those headless and omnicommerce tools (T.H.O.T.s) that enable SMB merchants to deliver delightful experiences to their end consumers.

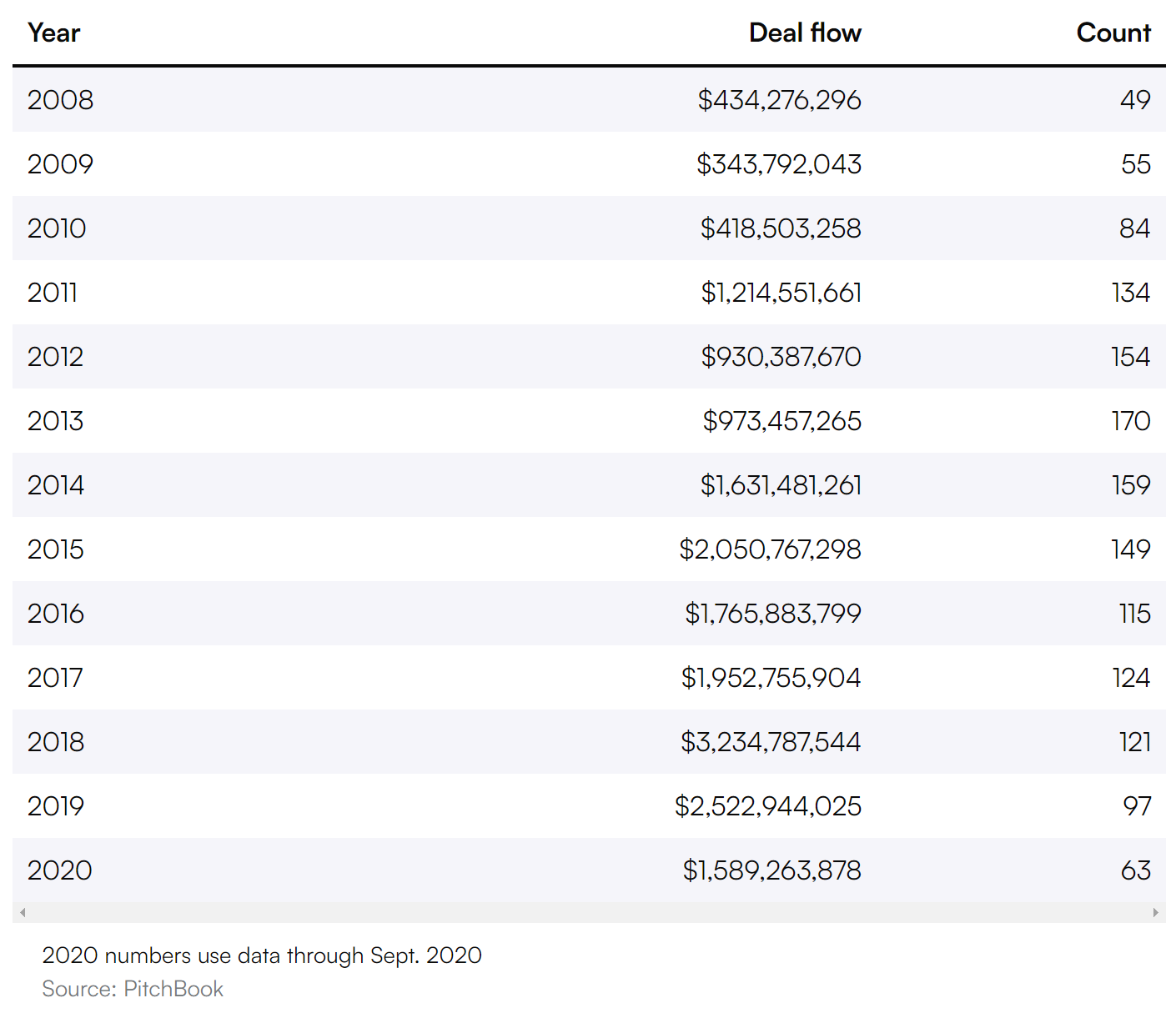

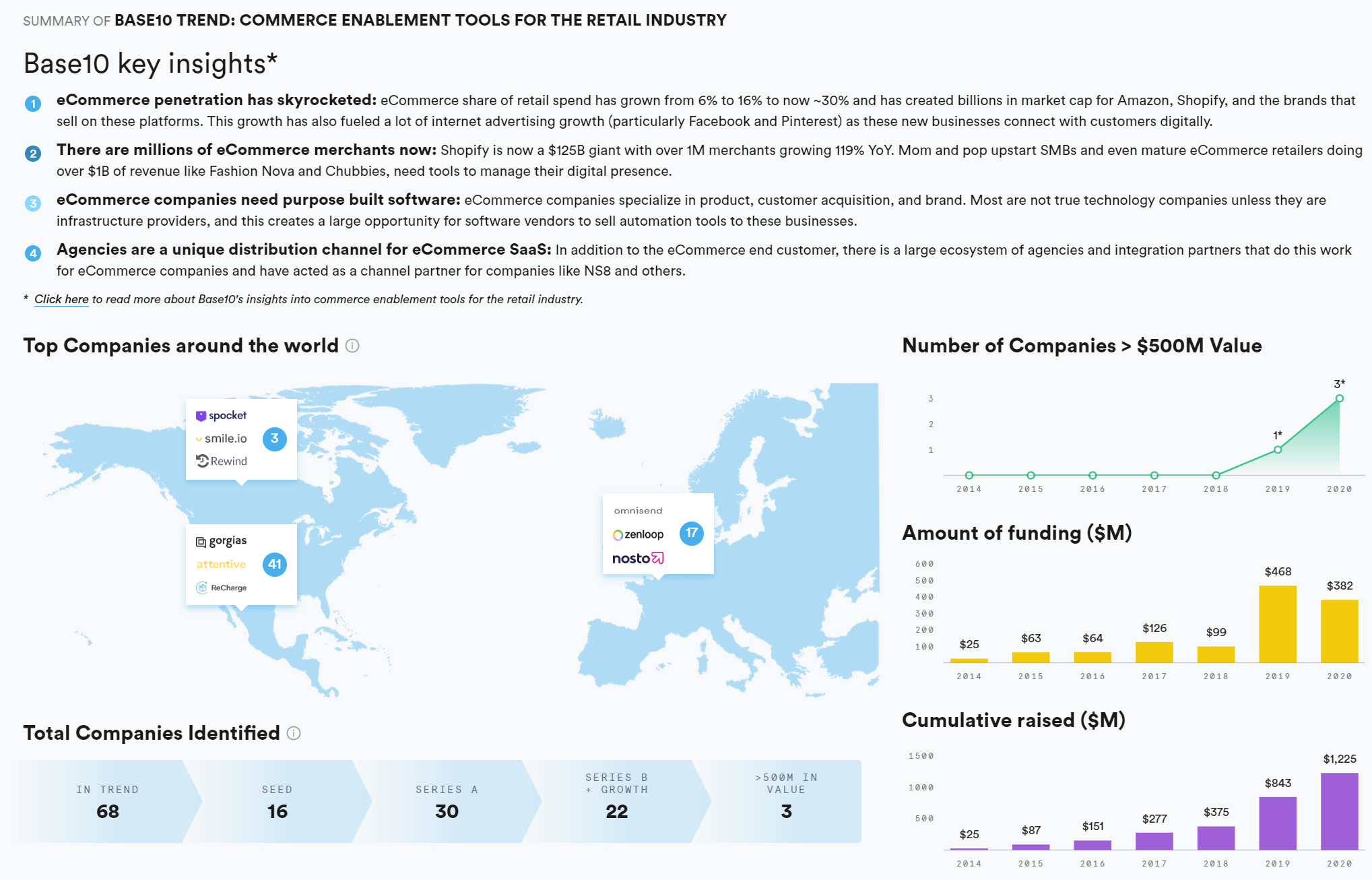

III. What is a T.H.O.T.? Headless commerce was coined by Dirk Hoerig as a necessary architectural framework for digitally driven commerce, requiring a break of defined limitations provided by traditional platforms. Simplistically, headless commerce architecture can be described as decoupling a website’s frontend presentation layer from its backend functional requirements which enables greater dynamism in pricing, infrastructure, security, consumer management, catalog, spend management, inventory management, and much more. Since Hoerig’s 2013 declaration of freedom to commerce, we’ve seen a proliferation of point solutions that would have once upon a time only been available to enterprise clients who could stomach the upfront and maintenance requirements of an ERP. The efficiencies of microservices technology, cloud compute, and open or quasi-open APIs offered by major platforms, enabled anyone from Microsoft to Post Imperial to reasonably offer best-in-class consumer experiences. Fabric, Cogsy, Shogun, Rally, mParticle, Northbeam, TripleWhale, Chord, Pack Digital, Segment, Gorgias, Klaviyo, Contently, Project44, Aftership, Recharge and much more… Of the thousands of companies we review, we track over 335 companies in commerce enablement that have received over $61 billion in VC dollars. Merchants’ desire for tools that bring them closer to their audience while giving them clear visibility across their operations continues to grow.

Similarly, omnicommerce is a term we have used to describe the next step of evolution in retail. It differs from omnichannel which is merely the recognition that brands are marketing their products through various retail distribution mechanisms. Omnicommerce, as defined by Daraa, refers to the always-on and everywhere nature of today’s store. Spellbound is putting a store in every email. Diagon is transforming capital equipment procurement in industrials. Fundamentally, the retail catalog has shifted online. Consumers are no longer perusing through magazines or newspapers to make informed buying decisions. After Apple ATT and Google’s cookie deprecation, existing playbooks and reliance on Facebook’s pixel have grown more challenging. THOTs have become more important as merchants need more flexibility to select the best tools for their needs and their consumers.

In the past, retail success was predicated on basic 4-wall economics. You establish a large retail fleet optimizing for payback period and $/sq ft. If you didn’t have the CapEx, you’d turn to wholesale under similar considerations. Then the DTC waive and Facebook’s Pixel augmented this reasoning. Take a look at the shift in performance and channel adopted by Ralph Lauren after the CEO replaced the founder in 2015. America’s largest luxury retailer leaned into its digitally driven retail strategy, that began a decade earlier and has resulted in 60% capture of its sales while shrinking its footprint. Ralph Lauren’s new way forward and the real and digital infrastructure required to make it work are indicative of where retail is headed. #OmniBaby!

At Stripe’s recent keynote, they set the commerce ecosystem ablaze with the announcement that they are ending the requirement that access to Stripe’s products requires a subscription to its payment processing. This move by Stripe highlights a move towards interoperability and a focus on their mandate to serve as financial infrastructure for the internet. Stripe is now much more than a PayFac, with a host of services that allow merchants to tackle the transactions pillar with ease. Deel, Ramp, Mercury Bank, and a handful of other startups are employing similar learnings as Stripe, building highly composable vertical OS that empower merchants to tackle their thorniest problems…

Enter Daraa. We’ve spent a lot of time listening to brands and evaluating how they want to show up for their audience. Daraa provides the real and digital infrastructure to arm brands and our communities with something more fulfilling...

Direct-to-consumer (DTC) evolved from a revolutionary model to just another retail channel. The rise of headless and omnicommerce tools (THOTs) empowers merchants to create flexible, customized solutions for online and offline channels. Successful brands now adopt an omnichannel approach, leveraging technology and data for personalized customer experiences.

.png)

.png)

.png)